{kind=link}

A senior citizen saving scheme is one of the best schemes in India if you are planning for a secured and stable income after retirement. This scheme has Government backing which implies that returns can be availed of in a hundred percent guaranteed manner; due its features of regular income and tax benefits, it is a great deal for the retirees as well.

This comprehensive blog will take you through everything you need to know about the Sr. citizen saving scheme such as the eligibility, features, benefits, how to apply and more – in an easy and simple language.

What is Senior Citizen Saving Schemes

Senior citizen saving scheme (SCSS) is a government-backed savings scheme specifically for the citizens above 60 years. Assist Retired Individuals With 0 Risks In Earning A Stable And Consistent Income After Retirement. It is also then open to all of us as this plan is available in post workplaces and approved banks across India.

Overview Table of Senior Citizen Saving Scheme

| Feature | Details |

| Scheme Name | Senior Citizen Saving Scheme (SCSS) |

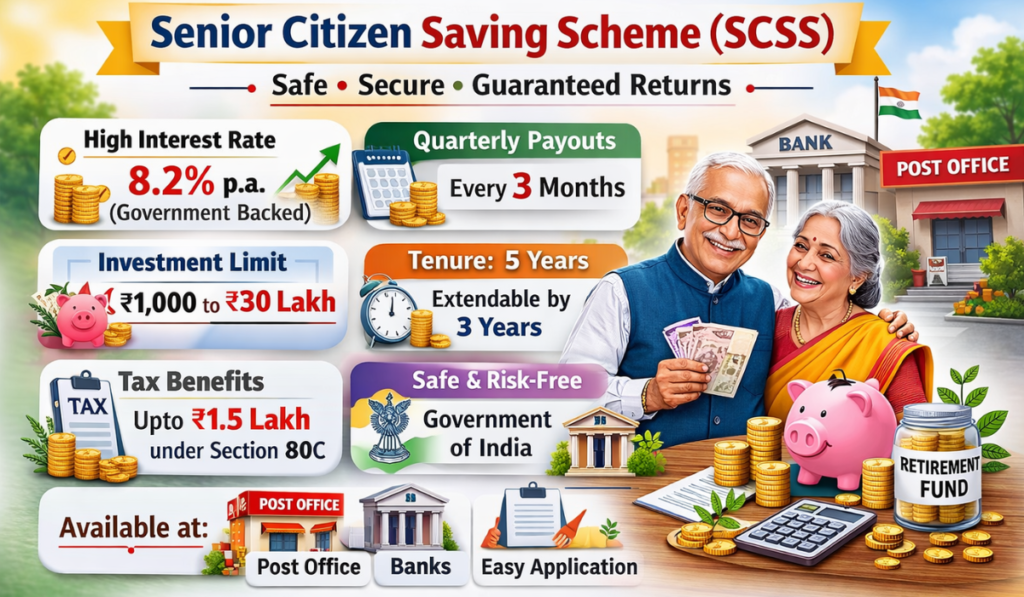

| Interest Rate | 8.2% per annum (2026) |

| Investment Limit | ₹1,000 to ₹30 lakh |

| Tenure | 5 years (extendable by 3 years) |

| Interest Payout | Quarterly |

| Risk Level | Very low (Government-backed) |

| Tax Benefit | Up to ₹1.5 lakh under Section 80C |

| Availability | Post Offices & Banks |

Key Features of Senior Citizen Saving Scheme

1. High Interest Rate

Currently offering an interest rate of around 8.2% per annum, the senior citizen savings scheme pays a higher rate than many traditional bank fixed deposits. It can be an ideal solution for seniors who want higher interest rates on their savings. The rate of interest is assessed by the government every quarter and is guaranteed to be competitive. Helps in keeping a constant income stream post-retirement.

2. Quarterly Income

The most significant benefit of this scheme is that quarterly interest payout. Such regular income is highly useful in meeting daily expenses post-retirement stage. Investors avoid waiting for maturity and get paid cash flow distributions on a regular basis. It offers financial planning simplicity and stability.

3. Investment Limits

The minimum investment for a senior citizen saving scheme is just ₹1,000, so it becomes possible for most common people to invest in it. The investment limit ranges from ₹20 lakh to ₹30 lakh, enabling retirees to utilize the larger portion of their retirement corpus. This flexibility enables them to opt for an amount based on their monetary affordability. It also safeguards more convenient financial security.

4. Tenure

It offers a fixed tenure of 5 years, aiding long-term planning and stability, be it a senior citizen saving scheme. Investors have the option of extending the account for 3 more years after the initial maturity. The extension option permits ongoing earning without requiring a new account. It is best suited for people who want safe investment but for a long period.

5. Government Safety

One of the safest investment options, the senior citizen saving scheme is government backed. You would not lose the capital like in market linked investments. Ideal for risk-averse seniors Its greatest strengths lie in safety and reliability.

6. Tax Benefits

The amount invested in the senior citizen saving scheme is eligible for tax deduction under section 80C of the Income Tax Act, upto ₹1.5 lakh. But the income earned is subjected to tax as per your income slab. That means upfront tax savings while you are investing. It is just a right mix of savings and return for retirees.

Benefits of Senior Citizen Saving Scheme

Here are the few benefits of the senior citizen saving scheme:

1. Guaranteed Returns

It comes with fixed interest with no market risk, and is best suited for conservative investors.

2. Regular Income Source

These quarterly payouts help in managing daily expenses after retirement.

3. Better Than FD

Superannuation contributions earn a better return than bank fixed deposits.

4. Tax Saving Advantage

You can claim deduction as taxable income under Section 80C

5. Easy Accessibility

You can get this at any post office and major banks in India.

Table

| Benefit | Short Explanation |

| Guaranteed Returns | Safe investment with fixed interest and no market risk |

| Regular Income | Quarterly interest helps manage daily expenses |

| Better Than FD | Higher returns compared to most bank fixed deposits |

| Tax Saving | Deduction up to ₹1.5 lakh under Section 80C |

| Easy Access | Available at post offices and banks across India |

Eligibility Criteria for SCSS

The following conditions must be complied with to open an account in a senior citizen saving scheme.

Basic Eligibility

- Persons that are 60 or older

- People who retired and aged 55-60 years (by VRS or any retirement benefit)

- Members of the defence force aged 50–60 years (subject to conditions)

- Not Eligible

- NRIs (Non-Resident Indians)

- HUF (Hindu Undivided Families)

- Note: Joint accounts are permitted, but the senior citizen should be the first holder in the account.

Detailed Explanation (In Simple Words)

It is a scheme meant to provide financial security to senior citizens post-retirement. Most people rely on savings after retirement, and SCSS gives them regular money every three months without having any concern about the market.

It is particularly beneficial for investors who prefer low-risk investments over high risk financial products like equities or mutual Funds. And because it is government backed your funds are fully secure.Even more significant is the interest rate, which now stands at 8.2%. This is many times better than traditional savings, making it possible for seniors to reap more on their savings.

In summary, SCSS offers a great mix of safety, returns, and periodic income, making it one of the best retirement schemes in India.The scheme currently offers around 8.2% interest, making it one of the highest among government savings schemes.

How to Apply for Senior Citizen Saving Scheme

1. Go to Your Nearest Post Office / Bank

You can initiate the investment in a senior citizen savings scheme through the nearest post office or any bank branch, which is permitted to offer this facility. This is an escrow scheme, which is widely available through most of the private and public sector banks in India. GM also asked the bank staff for how to join the scheme. This is the first step to start investing, the most important one.

2. Apply to SCSS

After you arrive at the post office or bank, you can complete the application for SCSS. This form will ask for your name, age, address, PAN number, and the amount you want to invest. Double-check that all the details are correct to prevent delays. There are always bank employees who can help you fill it out correctly.

3. Submit Required Documents

In addition to the filled form, it requires some important verification documents to be submitted. These include age proof (Aadhaar or PAN), identity proof, and address proof. This proved that you are eligible for a senior citizen saving scheme. Good documentation facilitates a seamless and stress-free account opening process.

4. Deposit the Investment Amount

After that you will go on to make a deposit with the value you want to invest in the said scheme. The minimum investment amounts to ₹1,000 and the maximum limit extends to ₹30 lakh. You can either deposit the money in-cash, by cheque or by bank transfer (depending on the institution). This sum will begin to attract interest in accordance with the rules of the scheme.

5. Nominate a Beneficiary

Lastly, always try to designate a beneficiary at the time of opening your SCSS account. This ensures that if something unfortunate happens to you, the amount you invested in will go to the family member that you choose. The nomination process is straightforward and can be edited later if required. It brings with it an additional level of confidence and financial security or peace of mind.

Read More:Agnipath Scheme: Complete Guide, Eligibility & How to Apply|Rajiv Yuva Vikasam Scheme 2026: Eligibility & How to Apply|PM Internship Scheme 2026: Complete Guide

Premature Withdrawal Rules

Allowed after opening the account Penalty applies:

- Before 1 year: No interest

- 1–2 years: 1.5% penalty

- 2–5 years: 1% penalty

Extension of Account

After 5 years:

- You can extend the scheme for 3 more years

- Interest rate will be applicable as per the current rate

Conclusion

Among the top government-supported investment options for retirees in India is a senior citizen saving scheme. With a promise of high interest, security and regular monthly income, it is ideal for a financially secure retirement. SCSS definitely deserves a place in your investment plan if you’re seeking a risk-free and income to earn with little hindrance.

FAQs Related to Senior Citizen Saving Scheme

Q1. What is the interest rate of the senior citizen saving scheme in 2026?

At this point, we offer the interest rate of ~ 8.2% per annum, paid quarterly.

Q2. What is the upper investment limit in SCSS?

The scheme allows the investment of maximum up to ₹30 lakh.

Q3 Is it possible that I take out money other than maturity?

Answer: Yes, but you will incur a fee based on the timing of the withdrawal.

Q4 Which one is better: SCSS or fixed deposit?

Yes, in most cases SCSS provide more interest and more safety than FDs.

Q5 Who is eligible for SCSS?

Eligible persons include those 60 years of age and older and qualified individuals who are retired 55+.

Q6 Is interest from SCSS taxable?

A: Yes, the interest is taxable, but under section 80C, you can claim deductions.

Q7 Are NRIs allowed to invest in senior citizen saving schemes?

If you are a Non Resident Indian (NRI), can you invest in SCSS? No, NRIs are not eligible to invest in SCSS.